The Ultimate Guide to Homeownership in Crivitz and Northeast Wisconsin

Buying a home in Northeast Wisconsin is unlike buying anywhere else. The properties here aren't mass-produced subdivisions with interchangeable floor plans — they're lakefront cabins, wooded retreats, century-old farmhouses, and rural parcels where the nearest neighbor might be a quarter mile down a gravel road. Each one comes with its own set of considerations: well and septic systems instead of municipal utilities, seasonal access roads, shoreland zoning restrictions, and heating systems built to withstand months of sub-zero temperatures. The buyers who thrive in this market aren't the ones who move the fastest. They're the ones who prepare the most thoroughly.

This guide walks you through every phase of the home buying journey, from assessing your finances and securing pre-approval to making an offer, navigating due diligence, and closing with confidence. Each section is built on the same strategy I use with every client I represent, a strategy shaped by my background in mortgage underwriting, which gives me a behind-the-scenes understanding of what lenders require, what can derail a loan at the last minute, and how to structure an offer that protects you financially. Whether you're a first-time buyer or relocating to the Northwoods from Green Bay, Milwaukee, or beyond, this checklist ensures nothing falls through the cracks. Let's get you home the right way.

Welcome Home!

Hi, I'm Alyssa Wennesheimer This checklist is your essential companion through the home buying journey. From first steps to closing day. Print it out, check off each step, and feel confident knowing exactly where you are in the process. Let's get you home.

Buying a home in Northeast Wisconsin, from the riverfronts of Niagara to the wooded retreats of Crivitz, requires more than just a standard checklist. It requires an understanding of our unique local landscape, seasonal shifts, and Northwoods property nuances. The homes up here aren't interchangeable. A lakefront cabin, a rural farmhouse, and a village starter home each come with their own considerations, from well and septic systems to shoreland zoning and seasonal access roads. I've helped buyers navigate all of it, and I'll help you do the same.

My background in mortgage underwriting means I see the transaction from both sides of the desk. I know what lenders require, what can derail a loan at the last minute, and how to structure an offer that protects you financially while keeping the deal on track. Whether you're a first-time buyer or relocating to the Northwoods, I'm here to make sure nothing catches you off guard.

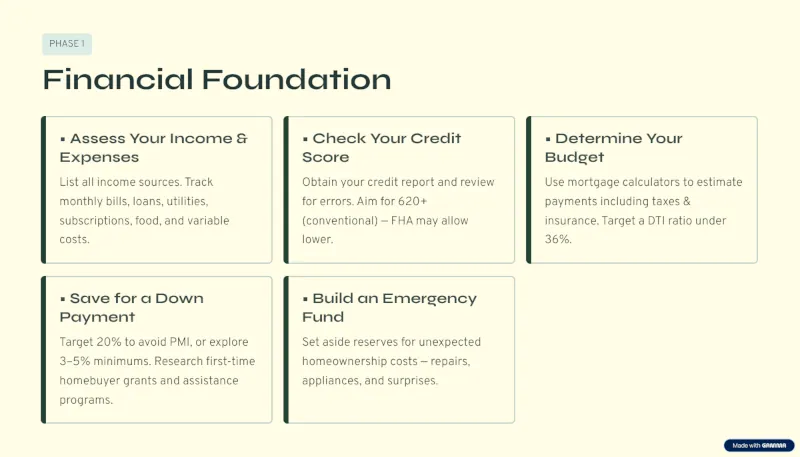

Phase 1: Building a Robust Financial Foundation

Before you fall in love with a property, you need to know exactly where you stand financially. A strong foundation isn't just about getting approved for a loan. It's about ensuring your monthly payment stays comfortable long after closing day. In Northeast Wisconsin, where property taxes and seasonal maintenance costs can shift unexpectedly, this phase is the difference between a home that builds your wealth and one that becomes a financial strain.

Comprehensive Income & Expense Assessment: List all income sources and track every monthly obligation such as bills, loans, utilities, subscriptions, food, and variable costs. Most buyers underestimate their monthly expenses by 15–20%. Knowing your true cash flow before you start shopping prevents the stress of a payment that barely fits your budget.

Credit Score Mastery: Obtain your credit report and review it for errors. Aim for a 620+ score for conventional financing. FHA programs may allow lower, but stronger credit unlocks better rates and lower monthly costs. Dispute any inaccuracies you find; even a small score improvement can save you thousands over the life of your loan.

Strategic Budgeting: Use mortgage calculators to estimate payments including taxes and insurance, not just principal and interest. Target a Debt-to-Income (DTI) ratio under 36%. This is the threshold most lenders use, and staying comfortably below it gives you breathing room for the unexpected costs that come with homeownership.

Down Payment Planning: While 20% down eliminates Private Mortgage Insurance (PMI), many programs allow 3–5% minimums. Research first-time homebuyer grants and assistance programs. Wisconsin offers several that buyers often overlook and I can help you identify which programs apply to your situation.

The "Surprise" Fund: Set aside reserves for unexpected homeownership costs. Things such as repairs, appliances, and surprises. This isn't optional; it's essential.

Why it matters in Northeast Wisconsin: In our region, "surprises" often come in the form of seasonal extremes. A robust emergency fund is vital for the Northeast Wisconsin spring thaw, which can reveal hidden driveway washouts or sump pump failures. Furthermore, with the 2026 Marinette County property tax referendum impacting local levies, having a clear understanding of your DTI is essential to ensure your monthly payment remains comfortable as local rates adjust.

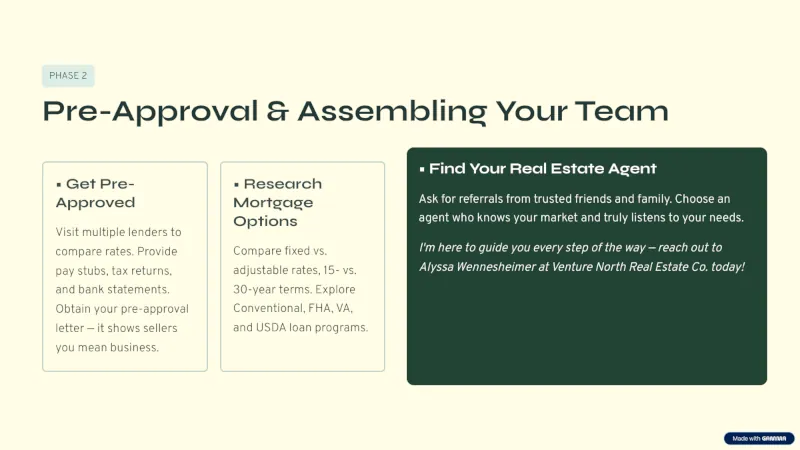

Phase 2: Pre-Approval & Assembling Your Team

Getting pre-approved isn't just a formality. It's your ticket to being taken seriously in a competitive market. Sellers want to see that a lender has already verified your finances, and a pre-approval letter tells them you're ready, willing, and able to close. But pre-approval is also your opportunity to shop the market and find the loan product that truly fits your situation, not just the first one you're offered.

Securing a Pre-Approval: Visit multiple lenders to compare rates and terms. You'll need to provide pay stubs, tax returns, and bank statements. Don't settle for the first approval you receive. Even a quarter-point difference in interest rate can save you tens of thousands over the life of your loan. Obtain your pre-approval letter and keep it current; most expire after 60–90 days.

Mortgage Product Research: Compare fixed vs. adjustable rates and 15- vs. 30-year terms to understand the trade-offs between monthly payment and total cost. Explore Conventional, FHA, VA, and USDA loan programs. Each has distinct advantages depending on your credit profile, military service, and property location. The right loan program can dramatically reduce your upfront costs and monthly obligation.

Partnering with a Local Expert: Ask for referrals from trusted friends and family. Choose an agent who knows your market and truly listens to your needs. I'm here to guide you every step of the way. Reach out to Alyssa Wennesheimer today!

Why it matters in Northeast Wisconsin: Much of Crivitz, Wausaukee, and the surrounding areas qualify for USDA Rural Development loans, which offer 0% down payment options for eligible buyers. Additionally, programs like WHEDA (Wisconsin Housing and Economic Development Authority) provide specialized down payment assistance and reduced interest rates specifically for "rural target counties" like Marinette County. A local expert with a background in mortgage underwriting can help you navigate these technical programs to maximize your savings. Because the right program isn't always the most obvious one.

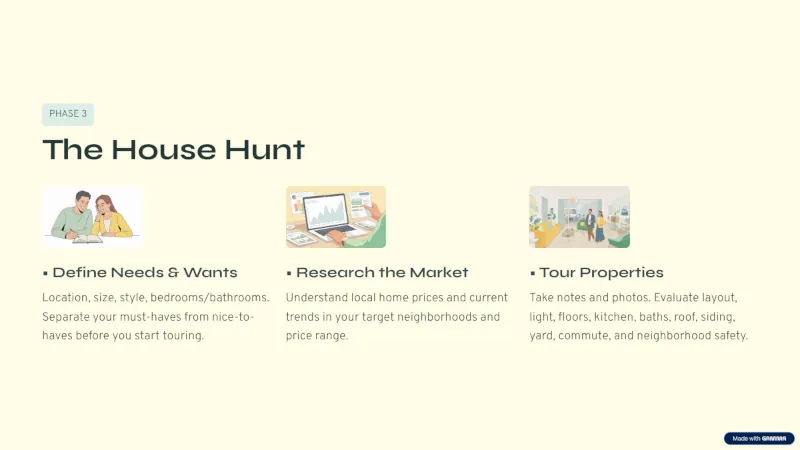

Phase 3: The Strategic House Hunt

The house hunt is where the excitement begins, but it's also where many buyers get overwhelmed by emotion. The key to success is discipline: separating your needs from your wants before you ever step foot in a property. In Northeast Wisconsin, where the landscape ranges from riverfront lots to wooded retreats, this clarity is your best defense against buyer's remorse.

Defining Needs vs. Wants: Create a list where you prioritize structural integrity over cosmetic finishes. A dated kitchen can be renovated; a cracked foundation or a failing roof cannot. Ask yourself: How many bedrooms do I truly need? Is a specific style non-negotiable, or just a preference? By defining these boundaries early, you save time and focus your energy on homes that actually fit your life.

Market Education: Understand the difference between a "Buyer's Market" and a "Seller's Market". In a buyer's market, you have leverage to negotiate price and terms. In a seller's market, speed and certainty are king. Knowing which side of the fence you're on helps you decide when to make a bold offer and when to wait for the right deal.

The Evaluative Tour: When you tour properties, take notes and photos, but look beyond the staging. Evaluate the layout, light, and flow, but also inspect the roof, siding, and natural drainage. Does the yard slope away from the house? Are there signs of water intrusion in the basement? These are the details that determine whether a home is a sanctuary or a money pit.

Why it matters in Northeast Wisconsin: The Crivitz real estate market currently shows a unique balance; while demand is high, homes often stay on the market longer than in urban hubs like Green Bay. This gives you more room to breathe during tours and less pressure to make impulsive decisions. However, you must pay close attention to Northwoods-specific features: Is the roof pitched correctly for heavy snow loads? Is the heating system (LP, electric, or wood) efficient enough for a harsh Wisconsin winter? A home that looks perfect in July might struggle in January if these systems aren't up to the task.

Phase 4: Making an Offer & The Art of Negotiation

Once you've found the right home, the real work begins: crafting an offer that gets accepted while protecting your interests. In Northeast Wisconsin, where the market can shift quickly between rural tranquility and competitive bidding, your offer strategy needs to be as precise as your search. It's not just about the highest price; it's about the smartest terms.

Calculating Your Offer: Base your price on local "comps" (comparable sales) and the home's current condition. Don't rely on Zillow estimates or emotional attachment. A data-driven approach ensures you aren't overpaying for a property that needs significant work, nor are you lowballing a well-maintained home and losing it to a competitor.

Protective Contingencies: Include financing, appraisal, and inspection clauses. These aren't just formalities; they are your exit ramps if something goes wrong. A financing contingency protects you if your loan falls through; an appraisal contingency ensures you don't owe more than the home is worth; and an inspection contingency gives you the leverage to request repairs or credits based on the home's actual condition.

Terms Negotiation: Work with your agent to reach a fair agreement on price, repairs, closing date, and more. Sometimes, a lower offer with a flexible closing date or a quick close can be more attractive to a seller than a higher offer with rigid terms. We negotiate for credits for repairs or closing costs to keep your cash flow healthy at the finish line.

Why it matters in Northeast Wisconsin: In rural transactions, your contingencies must go beyond the standard. It is critical to include a Well and Septic Contingency. Unlike city water, private systems in Northern Wisconsin must be tested for coliform bacteria, nitrates, and arsenic (sometimes lead). Negotiation in our area often includes these specialized inspections, ensuring you aren't inheriting a costly environmental or mechanical issue. A failed well or septic system can cost thousands to replace, making this contingency non-negotiable for any rural property.

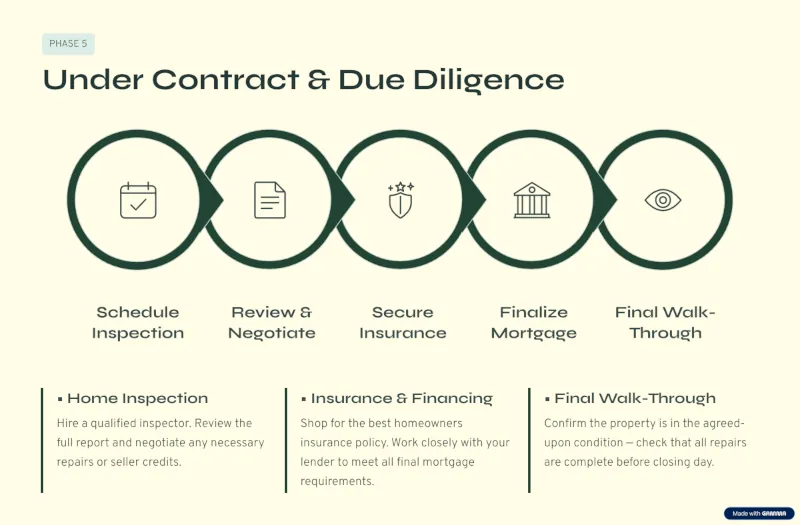

Phase 5: Under Contract & Due Diligence

Once your offer is accepted, the clock starts ticking. This phase is all about verification: ensuring the home is exactly what you think it is and that your financing is locked in tight. In Northeast Wisconsin, where the seasons dictate the condition of a property, due diligence isn't just a formality. It's your final line of defense against hidden costs.

The Home Inspection: Hire a licensed professional to check the foundation, roof, plumbing, electrical, and HVAC systems. Don't skip this step to save money; a thorough inspection can uncover issues that could cost you thousands later. Review the full report carefully and use it to negotiate necessary repairs or seller credits. This is your chance to address problems before you take ownership.

Finalizing Financing & Insurance: Shop for the best homeowners insurance policy and work closely with your lender to meet all final mortgage requirements. Your loan isn't fully approved until you've secured insurance and provided all requested documentation. Stay responsive to your lender's requests to avoid delays that could jeopardize your closing date.

The Final Walk-Through: Confirm the property is in the agreed-upon condition. Check that all negotiated repairs are complete, the home is empty (unless otherwise agreed), and no new damage has occurred since your last visit. This is your last opportunity to ensure everything is in order before you sign the final papers.

Why it matters in Northeast Wisconsin: During the Wisconsin Spring Market, an inspection should specifically target "winter wear." Look for ice dam damage in the gutters or frost heave in the foundation, which can compromise structural integrity. Because many properties in the Crivitz area serve as seasonal homes, your due diligence should also verify that the home was properly winterized if it sat vacant during the colder months. A poorly winterized home can suffer from burst pipes, frozen tanks, and mold growth. These issues that are expensive to fix and often missed by a cursory inspection.

Phase 6: Closing Day

Closing day is the finish line, but it's not a rubber stamp. This is your last chance to catch errors, confirm your terms, and make sure the numbers match what you agreed to. By the time you sit down at the closing table, there should be no surprises. It should be just signatures, a handshake, and the keys to your new home.

The Closing Disclosure (CD): Carefully review all final costs, fees, and loan terms before you sign anything. Your lender is required to provide the CD at least three days before closing. Compare every figure against your Loan Estimate. If the interest rate, monthly payment, or closing costs have changed significantly, raise the question immediately. This is not the time to rush; a single overlooked fee can cost you for decades.

Signing & The Handover: Complete all necessary legal documents with your agent and closing attorney or title company. You'll review and sign the deed of trust, promissory note, and settlement statement, among other documents. Once everything is recorded and funded, you'll receive your keys. Congratulations! You're officially a homeowner! Welcome home.

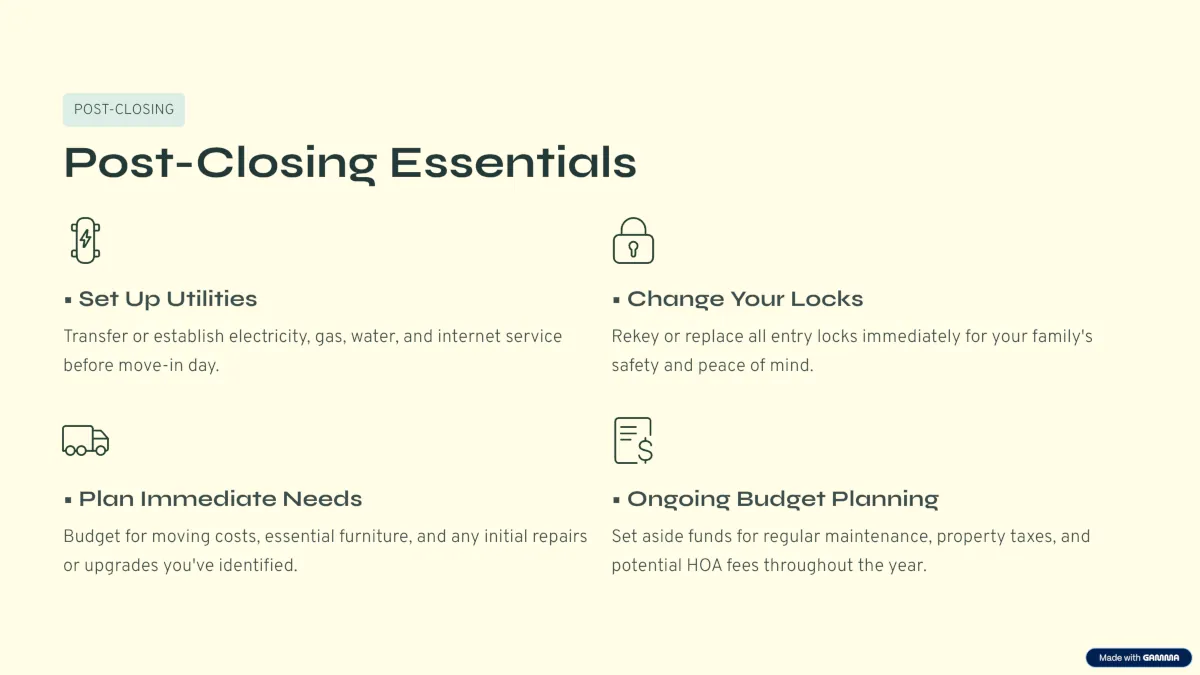

Post-Closing Essentials

The work doesn't end at the closing table. Transfer utilities into your name and rekey your locks immediately. These tasks are easy to overlook in the excitement of moving day, but they're critical for both convenience and security.

Why it matters in Northeast Wisconsin: In our tight-knit community, local utility transfers (like those for Crivitz or Niagara municipal services) are best handled a week in advance. Small-town utilities don't always operate on the same timeline as larger providers, and a delay could mean arriving at your new home without water or electricity on day one. For Northwoods safety, rekeying your locks on day one is essential, especially for properties that may have had multiple contractors or seasonal renters in the past. You don't know who still has a key, and in a rural area where neighbors may be miles away, securing your home is a priority, not an afterthought.

Ready to Start Your Northwoods Journey?

Buying a home is one of the most exciting milestones of your life and you don't have to do it alone. Whether you're searching for a forever home or a weekend retreat, I'm here to guide you through every phase of this journey with expertise, care, and commitment. From your first financial assessment to the moment the keys are in your hand, I treat your purchase the way I'd want my own handled: with precision, transparency, and zero surprises.

What sets my approach apart is simple: I bring technical expertise and local passion to every transaction. My background in mortgage underwriting means I understand the financing side from the inside out — I know what lenders require, what can stall a loan, and how to structure an offer that holds together under scrutiny. Combined with deep roots in the Crivitz and Marinette County market, I ensure you're not just buying a house, but making a sound investment in the right property for your life.

The Northwoods isn't just a place to live, it's a lifestyle. From the shores of the Peshtigo River to the ATV trails winding through Marinette County, this community offers something you won't find anywhere else. I know because I chose it myself. Let me help you find your piece of it.

Ready to get started? Let's talk about your goals, your timeline, and the plan to get you home.